What are the best CD interest rates going into 2026?

As 2025 draws to a close, many individuals are reflecting on their financial health and setting new goals for the year ahead. Whether you’ve been diligently saving, navigating a period of significant spending, or simply maintaining a steady course, one universal truth for all savers is the imperative to safeguard and grow their funds effectively in 2026. While the desire to achieve this is common, the path to successful execution can often be less clear. Fortunately, Certificate of Deposit (CD) accounts continue to offer a robust and predictable avenue for wealth accumulation, even if the interest rates they offer have seen some moderation compared to the peaks of recent years.

CD accounts currently boast average interest rates that remain significantly higher than those typically associated with traditional savings accounts. A key differentiator and a major advantage of CDs is their fixed interest rate structure. Unlike the variable rates found in traditional or high-yield savings accounts, the rate you lock in today, in the waning weeks of 2025, will remain constant throughout the entire term of your CD until it reaches maturity. This inherent predictability is a powerful tool for financial planning. It not only simplifies the process of calculating precise interest earnings but also provides savers with a clear foresight into their investment growth, a level of certainty that simply isn’t available with alternative variable-rate options.

To fully grasp the benefits and potential of CD accounts as we transition into 2026, it’s essential to understand what constitutes the "best" CD interest rates across various popular terms. Below, we’ll delve into the top rates currently available for six common CD durations and illustrate the potential earnings from a $10,000 deposit into each.

The Evolving Economic Landscape and CD Rates

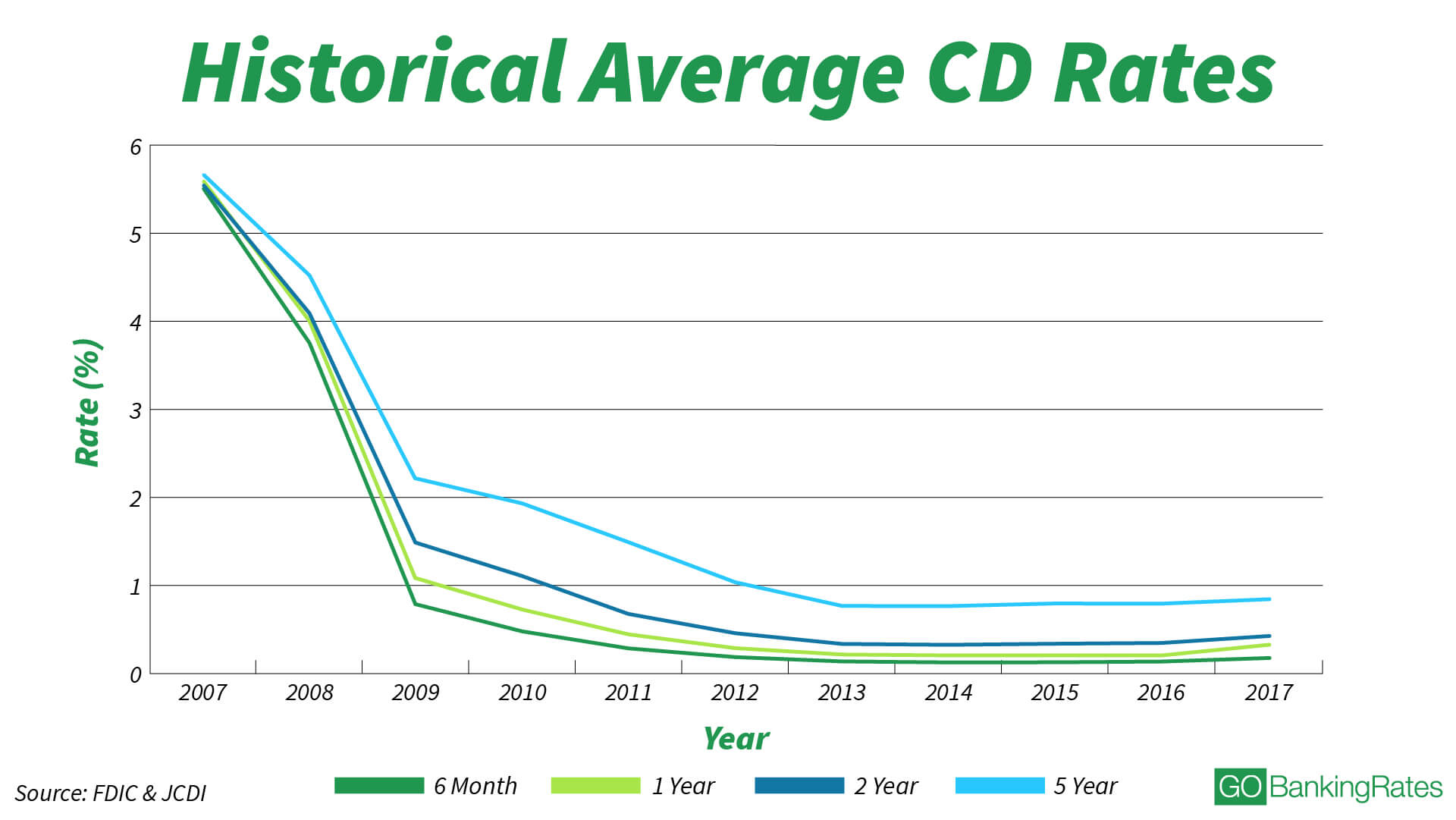

The trajectory of CD interest rates is intimately tied to the broader economic environment, particularly the Federal Reserve’s monetary policy decisions. In recent years, central banks worldwide, including the Fed, implemented aggressive interest rate hikes to combat surging inflation. This period saw CD rates soar, offering savers some of the most attractive returns in decades. As inflation has shown signs of cooling and the economy adjusts, the Fed’s stance may shift towards a more neutral or even accommodative policy, which could influence future rate movements.

Going into 2026, experts generally anticipate a more stable, though potentially slightly lower, interest rate environment compared to the recent highs. While the era of rapidly rising rates might be behind us, current CD rates still represent a compelling opportunity, especially when contrasted with the near-zero rates offered by conventional savings accounts. The fixed nature of CDs also offers a hedge against potential future rate declines, allowing savers to lock in today’s favorable rates for an extended period. This makes them an attractive option for those seeking stability and guaranteed returns amidst ongoing economic uncertainties.

Understanding CD Terms and Their Potential Earnings Going Into 2026

Contemplating opening a CD account now? Here are some of the highest rates you’re likely to find for some common CD terms, along with estimated earnings on a $10,000 deposit:

3-Month CD Accounts

For savers seeking short-term security and a modest return, a 3-month CD offers an excellent solution. This option is ideal if you anticipate needing access to your funds relatively soon but want to keep them working for you in the interim. The best 3-month CD rates currently range between 3.85% and 4.00% Annual Percentage Yield (APY).

- Estimated Earnings on $10,000: With a rate of 3.95% APY, a $10,000 deposit could earn approximately $98.75 over three months.

- Suitability: Perfect for parking emergency funds that need to be liquid within a quarter, or for short-term savings goals where immediate access isn’t critical but a small return is desired. It provides a brief period of fixed growth before you regain control of your capital early in 2026.

6-Month CD Accounts

If you’re willing to commit your funds for a slightly longer period, a 6-month CD often comes with a more competitive interest rate, translating to greater earnings. These accounts strike a balance between short-term liquidity and enhanced returns. Current top rates for 6-month CDs typically fall in the 4.05% to 4.20% APY range.

- Estimated Earnings on $10,000: At a 4.15% APY, a $10,000 deposit could yield around $207.50 over six months.

- Suitability: A good choice for mid-year savings goals or for those who want to take advantage of current rates for a reasonable period without tying up their money for too long. It offers a noticeable improvement in earnings compared to the 3-month option, providing a healthy return per hundred dollars deposited.

9-Month CD Accounts

A 9-month CD account provides protection for your money through a significant portion of the coming year, often with attractive rates. This term is particularly appealing for those exploring a CD laddering strategy, which involves staggering multiple CDs with different maturity dates. Top rates for 9-month CDs are generally between 3.95% and 4.15% APY.

- Estimated Earnings on $10,000: Utilizing a 4.05% APY, a $10,000 deposit could accrue approximately $303.75 over nine months.

- Suitability: Ideal for specific financial milestones planned for the end of Q3 2026, or as a component of a CD ladder. This duration offers a balance of higher earnings and moderate liquidity, allowing for strategic access to funds at different points throughout the year.

1-Year CD Accounts

For those looking to secure their money until late next year, a 1-year CD account is a popular and effective choice. These accounts typically offer a solid balance of rate competitiveness and a manageable term length. The best 1-year CD rates currently hover in the 4.05% to 4.10% APY range.

- Estimated Earnings on $10,000: With a rate of 4.08% APY, a $10,000 deposit would earn approximately $408.00 over the full year.

- Suitability: This is a benchmark CD term, suitable for a wide range of savers. It’s particularly good if you have a lump sum you won’t need for exactly one year, perhaps for a future down payment, tuition payment, or a large purchase. The key is ensuring you can keep your funds untouched for the entire year, as early withdrawal penalties on a 1-year CD can significantly erode your interest earnings.

18-Month CD Accounts

For extended protection and growth, an 18-month CD account presents a compelling option. While the rates might be slightly lower than some shorter terms due to expectations of future rate changes, the longer compounding period can result in higher overall interest earned. The best rates for 18-month CDs are typically in the 3.95% to 4.05% APY range.

- Estimated Earnings on $10,000: Assuming a 4.00% APY, a $10,000 deposit could generate approximately $600.00 over 18 months.

- Suitability: This term is excellent for medium-term savings goals that extend beyond a year but don’t require a multi-year commitment. Examples include saving for a car, a significant home improvement project, or a large vacation. The extended timeline allows for more substantial interest accumulation compared to shorter-term CDs, even with marginally lower rates.

2-Year CD Accounts

Looking ahead to November 2027 might seem distant, but for savers who prefer a "set it and forget it" approach to a portion of their money while still earning a decent return, a 2-year CD is worth investigating. The best rates for this account term currently sit between 3.95% and 4.00% APY.

- Estimated Earnings on $10,000: At a 3.98% APY, a $10,000 deposit could earn approximately $796.00 over two years.

- Suitability: This term is best for long-term savings goals where liquidity is not a concern for a full two years. However, the early withdrawal penalty for a 2-year CD can be quite substantial, often equivalent to several months of interest. Therefore, it’s crucial to be absolutely certain you won’t need access to these funds for the entire 24-month period. It offers the highest overall interest earnings among the terms discussed, assuming the funds remain untouched.

Beyond Single CDs: The CD Laddering Strategy

While individual CD accounts offer clear benefits, a sophisticated strategy known as CD laddering can enhance both your returns and liquidity. CD laddering involves dividing your total savings into multiple CDs with varying maturity dates. For example, instead of putting $10,000 into a single 2-year CD, you might invest $2,500 into a 6-month CD, $2,500 into a 1-year CD, $2,500 into an 18-month CD, and $2,500 into a 2-year CD.

As each shorter-term CD matures, you can then reinvest that money into a new, longer-term CD (e.g., a new 2-year CD). This strategy provides several advantages:

- Enhanced Liquidity: You have a portion of your money becoming available at regular intervals (every 6 months in the example), offering greater flexibility than a single long-term CD.

- Rate Averaging: You benefit from potentially higher long-term rates while also having funds mature regularly to capitalize on any rising rate environments. If rates fall, you still have some funds locked into older, higher-rate CDs.

- Reduced Risk: You mitigate the risk of locking all your money into one rate that might become less competitive if rates rise significantly.

This strategy allows you to maintain a continuous stream of maturing funds, providing both access to capital and the opportunity to consistently earn competitive interest.

How to Choose the Best CD for You

Selecting the right CD involves more than just picking the highest rate. Consider these factors:

- Your Time Horizon: How long can you comfortably lock away your money without needing it? Match the CD term to your financial goals.

- Liquidity Needs: Do you anticipate needing access to funds unexpectedly? If so, shorter-term CDs or a CD ladder might be more suitable. Remember, early withdrawal penalties can be steep.

- Interest Rate Outlook: While rates are fixed, your perception of where rates might go could influence your term choice. If you expect rates to rise, shorter terms allow you to reinvest sooner. If you expect them to fall, longer terms lock in today’s higher rates.

- Minimum Deposit Requirements: Some CDs, especially those with top rates, may require a higher minimum deposit.

- Bank Reputation and FDIC Insurance: Always ensure your CD is held at an FDIC-insured institution. This guarantees your deposits up to $250,000 per depositor, per institution, in case of bank failure.

The Bottom Line

While CD interest rates may not be reaching the stratospheric highs observed in the very recent past, they remain remarkably competitive and offer a compelling value proposition for discerning savers. Going into 2026, CD accounts continue to provide a secure environment for your capital, coupled with guaranteed interest earnings. If your financial objectives include certainty of return, a willingness to keep funds untouched for a specified period, and a desire to avoid the complexities and volatility of constantly changing market rates or investment landscapes, a Certificate of Deposit account emerges as a highly viable and attractive option. Explore the current offerings now, and make an informed decision to strengthen your financial position in the year ahead.